It often starts small. A customer moves money into their Skrill account - nothing unusual. Just a simple transaction in the background of an otherwise quiet banking day. But hours later, that same payment is funneled into an online casino, masked by a generic merchant category code. On the surface? Innocent. Behind the scenes? Potential risk.

What is Skrill?

Skrill is a digital wallet and payment platform used for online money transfers, shopping, and deposits to gambling sites. While it’s a legitimate financial service, Skrill is commonly used by customers to fund online betting accounts, making it a key intermediary in gambling transactions. Because it operates under a broad MCC 6012, traditional banking systems often fail to detect its connection to gambling activity.

For banks, it’s time to focus on the human aspect of gambling, not simply transactional. Spotting gambling behavior is about understanding the story behind the transaction and offering better support before things spiral. That’s why financial institutions must go beyond outdated classification methods and look for advanced data enrichment techniques.

The Challenge of Detecting Gambling

MCCs are four-digit numbers that merchants use to classify their primary business activities. While many gambling-related transactions are categorised under MCC 7995 (Betting, including Lottery Tickets, Casino Gaming Chips, Off-Track Betting, and Wagers at Race Tracks), this system has notable limitations. It was designed for interchange fees, not categorisation. Gaps include:

- Alternative MCC Usage: Merchants may register under different MCCs to avoid the penalty associated with gambling activities. For instance, a gambling platform might use MCC 7994 (Video Game Arcades) to obscure its true nature.

- E-Wallets and Payment Gates: Transactions processed through e-wallets like Skrill or Neteller often appear under MCC 6012 (Financial Institutions – Merchandise and Services), making it challenging to identify the underlying gambling activity.

- Cryptocurrency Platforms: Some gambling sites accept cryptocurrency deposits, which can be processed through exchanges categorised under MCC 6051 (Non-Financial Institutions – Foreign Currency, Money Orders). This indirect pathway further complicates detection efforts.

Did you know?

According to BIT's 2023 study, 60% of online gamblers deposit funds from a single bank account, meaning that even small-scale gambling behavior can accumulate and go unnoticed by banks that lack accurate data.

The biggest problem in spotting these transactions is what happens if they go unnoticed. Regular gambling activity can signal financial distress, impact trustworthiness, and affect a bank’s decision to extend credit or offer premium financial services. For financial institutions, these gaps in detection lead to two major risks: false positives and false negatives.

Flagging legitimate transactions as gambling can frustrate customers and create unnecessary restrictions, while failing to detect actual gambling transactions exposes banks to regulatory violations and increased financial risk. But instead of demonising gambling or stopping it outright, banks should help customers manage their behavior in ways that don’t put them at financial or emotional risk. That starts with data.

A New Approach: Transaction Data Enrichment

Instead of focusing solely on MCCs, transaction enrichment uses AI and behavioral analytics to dig deeper. It cross-references merchant names, payment pathways, time-of-day patterns, and historical behaviors. Over time, it learns to identify the “where” and “why” of each transaction.

Take our Skrill example again. One transfer might not mean much. But if a customer consistently uses Skrill before late-night spikes in spending - and those funds align with known gambling merchant fingerprints - banks can flag that pattern as potentially risky. It’s about awareness. It helps banks provide support where it’s needed, and just as importantly, avoid overreaching where it’s not.

Why? Because it’s not always gambling. You don’t want to tell a customer their MMO game subscription looks suspicious. And yet, that happens when banks rely solely on MCC codes like 7995. This one code is used for both gambling websites and video games with paid content or fantasy sports features.

Here’s what makes that messy:

- A gamer subscribing to World of Warcraft might get flagged

- Someone buying FIFA Ultimate Team points could get caught in a false positive

- Even a casual player on a fantasy sports platform might get labeled a high-risk gambler

That’s a recipe for customer churn. Enriched data reduces this risk by matching merchants and context. It sees when a payment is going to an online game server versus a crypto-backed betting site. That means fewer embarrassing flags and more informed, confident customer experiences.

What Should Banks Actually Do?

They could block all suspicious transactions - but let’s be honest, that often backfires. Customers find workarounds. Or worse, they leave for fintechs with fewer restrictions. Instead, enrichment allows banks to adopt a more collaborative approach.

Did you know?

BIT’s study found that adding spending limits instead of blocks increased gambling management tool usage by 6 to 11 %.

UK banks like Monzo, Starling, and HSBC are already doing this. They’ve implemented optional gambling blocks, 48-hour reactivation delays, and budgeting nudges - all designed to empower users, not punish them. With Monzo for example, almost 100,000 people have used it in 2023 and blocked more than 200,000 attempted gambling transactions.

Compliance With Compassion

Let’s talk regulation. Banks have a responsibility to comply with AML (anti-money laundering) and CTF (counter-terrorist financing) laws. And gambling is often flagged as a high-risk activity in these contexts.

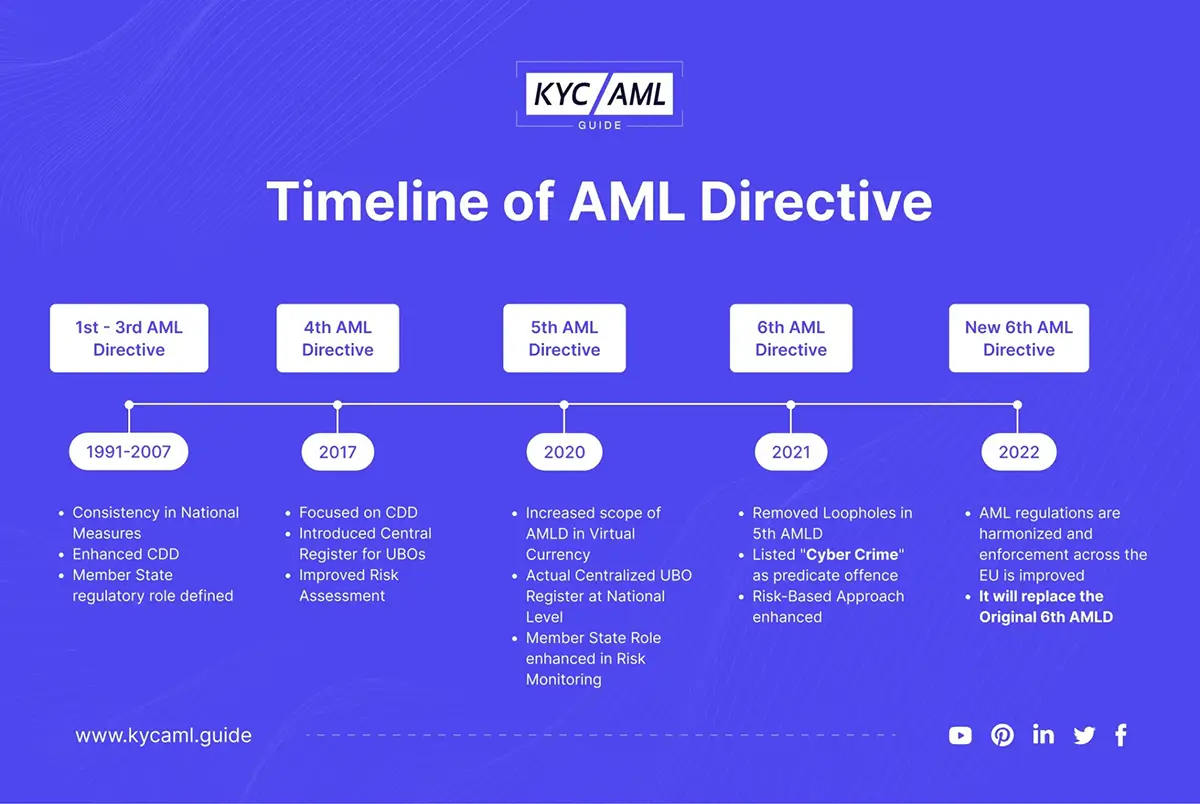

Since its inception in 1991 (but most notably from 2017 onwards), all new European directives (such as The Sixth Anti-Money Laundering Directive, The Markets in Crypto-Assets Regulation and The EU Single AML Rulebook) called for even stricter oversight on digital payments, especially involving crypto, e-wallets, and cross-border transfers. That means stricter scrutiny of merchant types, higher standards for identifying the purpose of funds and increased fines for letting money slip through undetected.

Enriched transaction data helps banks meet these demands - without alienating users. Instead of broad-stroke restrictions, they can apply targeted interventions. Instead of fear-driven policies, they can embrace insight-driven strategies.

Smarter Detection Boosts the Metrics That Matter

For banks, supporting customers with better gambling oversight means both doing the right thing and hitting the right numbers in the process. Because once you integrate enhanced transaction data and rethink how you engage with gambling behavior, several core performance metrics start to shift for the better.

Higher Customer Satisfaction: False positives are one of the biggest friction points in digital banking. Accidentally blocking a game subscription or flagging a fantasy football payment as risky can quickly drive the users away. Enrichment reduces those mismatches, improving the accuracy of flagged transactions and keeping loyal customers from jumping ship.

Did you know?

Capgemini’s 2023 World Payments Report found that 37% of banking customers who experienced a wrongful transaction decline switched providers within six months.

Improved Engagement with Financial Tools: Adding voluntary features like gambling blocks or spending limits actually deepens customer engagement. Instead of avoiding their banking app, users check in more often, use budgeting tools, and build a more transparent financial relationship with their bank.

Did you know?

A 2023 trial by the BIT found that introducing gambling spending limits increased customer use of financial management tools by 6 - 11 %.

Lower Risk Exposure: Anti-money laundering compliance focuses on passing an audit but also avoiding unpleasant penalties. With enriched transaction data, banks can not only identify these transactions but also prove their oversight, satisfying regulators and reducing exposure to compliance fines.

Did you know?

The gambling industry faced fines exceeding $69 million for AML breaches in 2024. For instance, Crown Resorts faced a $450 million penalty for failing to assess money laundering risks at its casinos.

Higher Operational Efficiency: Friendly fraud and dispute-prone gambling transactions create unnecessary operational strain. With merchant-level insights from enriched data, banks can reduce fraudulent chargebacks and back up legitimate declines, saving hours of back-office resources and avoiding unnecessary losses.

Did you know? Online casinos and sportsbooks experience high chargeback rates averaging between 2% to 4%, attributed to unauthorised use of stolen cards and disputes over transactions.

Today’s financial institutions need deeper insights - insights that only enriched transaction data can provide. Whether it’s uncovering hidden gambling transactions within e-wallet payments, distinguishing between legitimate gaming expenses and betting, or tracing crypto deposits linked to online casinos, enriched data enables banks to see the full picture.