For many decades, credit scoring has built the foundation of financial risk assessment and provided banks and other financial institutions with a quantitative view of a borrower's creditworthiness. Traditionally, credit scores are derived from a combination of factors that include payment history, credit utilization, the length of credit history, types of credit used, and recent credit inquiries. These data points offer a very narrow window into the financial behavior of a borrower and often lead to misjudgments in lending decisions. A modern answer to this is smart data. Or, more precisely, enriched data.

Do You Know Who You're Lending Money To?

.webp)

Relying solely on traditional methods of credit scoring today is comparable to trying to get around with a map from the 1800s. The dynamics of personal finances do call for a more solid and detailed approach. And by that, we mean enriched data for credit scoring, which is the next evolutionary step in assessing financial risk by incorporating various data points and offering an all-rounded, personalised view of a borrower's financial behavior.

Did you know? According to SP Global, approximately 40% of lower-rated credits in Europe are at risk of downgrades in 2024 due to economic pressures and tightening financing conditions.

Various credit scoring models, such as FICO, Equifax, Experian, TransUnion, and other regional systems, each use slightly distinct algorithms and criteria to evaluate creditworthiness. Despite these differences, a common thread among them is the critical importance of transaction history. This data, which includes details on spending habits, debt repayments, and overall financial behavior, is fundamental to accurately assessing an individual's credit risk. For instance, FICO scores heavily weigh payment history and amounts owed, while Equifax incorporates the alternative data sources, such as utility payments, rent payments, and employment information. This emphasis on transaction data shows how important the process of enrichment is and how it affects the accuracy, and usefulness of that data.

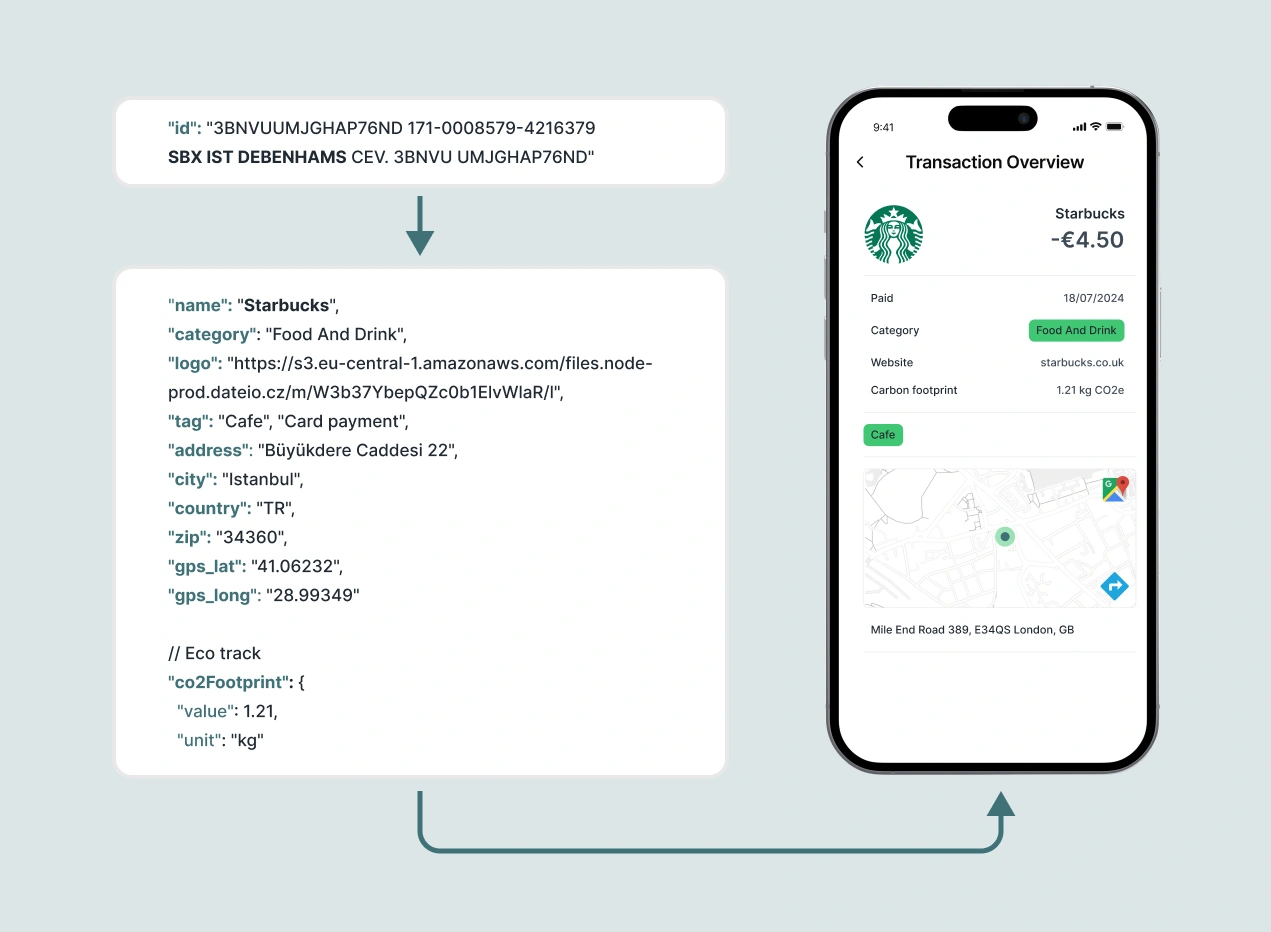

One of the critical components of smart data is accurate payment categorisation. Traditional methods, which rely on MCC codes, often fall short, with studies showing that more than a third of all categorisation data is incorrect. This inaccuracy can lead to flawed credit assessment, and a high financial strain for banks.

Advanced categorisation, backed up by enriched transaction data, goes beyond MCC codes. It uses over 500 tags at the shop level and 25 main categories at the merchant level, ensuring detailed and precise labelling. This approach enables financial institutions to understand not just where money is spent, but also the nature and context of the expenditure.

Benefits of Enhanced Credit Scoring

Enhanced credit scoring with smart data significantly lowers default risk rate, in some cases by up to 30% according to a study by the Federal Reserve. Enriched data can hold indicators that otherwise may not turn up in predictive models built from traditional sources and helps a bank take appropriate mitigation measures against risk. For example, frequent transactions in high-risk areas or recurring payments for services that indicate financial strain can be early indicators of credit risk.

Besides lowering default risk rate, enriched data offers several other advantages:

Enhanced end-user engagement: More accurate data means better performing PFM with a clear transaction overview and history. According to a survey by The Clearing House, users who receive detailed transaction histories and financial insights report higher engagement with their financial apps.

More accurate behavioural analysis: Enriched data allow a better understanding of spending patterns and habits, as well as recurring payments and subscriptions. This gives banks a deeper understanding of a client’s financial behavior and their financial journey in general, while also adding informational value to the client while using the bank apps.

Real-time credit scoring: The ability to process and analyze data in real-time is a significant advantage. For example, the Tapix enrichment platform can return data within 6 milliseconds, allowing for instant credit-scoring decisions. In the context of Buy Now, Pay Later (BNPL) services, the actual speed of data enrichment plays an important role. BNPL providers rely on instantaneous credit assessments to approve transactions at the point of sale. The ability of tools like Tapix to deliver enriched data with only a few milliseconds delay ensures that the entire process remains nearly seamless.

Increased card usage: If clients know where they spend their money, it gives them the initiative to use the account as their primary bank. This leads to increased card usage, higher user deposits and more opportunities for upselling. More card transactions provide more data, which, in turn, refines the credit scoring models, creating a positive cycle.

Behavioral Patterns and Their Impact on Credit Scoring

Understanding behavioral patterns is crucial for accurate credit scoring. For instance, a customer who frequently dines at high-end restaurants may have a different risk profile compared to someone who primarily shops at discount stores. Banks should be in a position to recognize such patterns and make much more targeted credit offerings with correspondingly less risk.

Another example is recognizing customers with a large number of small-value loans that may highlight their suffering from financial stress, while those with few large-value loans and a history of timely repayments would point toward good financial health. Or spending by a customer consistently at expensive grocery stores may be of a different risk profile compared to one frequently shopping at discount stores.

Did you know? 44% of surveyed cardholders mistakenly believe that carrying a credit card balance helps improve their credit score. In reality, paying off balances in full is better for credit health.

Let's take a look at some behavioral patterns and unique types of cases smart data can help with:

Big spender - Individuals who consistently make high-value purchases, whether on luxury items, dining out at upscale restaurants, or frequent travel. Their financial focus is often on maintaining a lifestyle that reflects their income and social status. In the case of big spenders, credit scoring zeroes in on finding the ability, capacity, and efficiency to handle large amounts of credit and repay the same. Enriched data helps to underline the spending pattern and financial habits, ensuring that their high spending does not translate necessarily into a high risk.

Family member/Parent - Often characterized by regular spending on household needs, education, and healthcare, they always prioritize stability and financial planning in the long term. Credit scoring to such groups include steady income, regular expenses, and financial responsibilities that come with managing a household. Enriched data reveal the existence of stable and predictable consumption patterns, as well as the use of credit responsibly, with banks offering appropriate credit products, such as home or education loans.

Student - Students usually have limited credit history and irregular income, often relying on part-time jobs, allowances, or student loans. Their financial priority is to be able to manage educational expenses in balance with living costs. Credit scoring for students must adapt to their unique situation, often emphasizing alternative data points like timely payment of utility bills or rent. Enriched data go far beyond traditional credit metrics, allowing lenders to design tailor-made financial products such as student credit cards or low-interest emergency loans.

Retiree - Retirees typically have a fixed income from pensions, savings, or investments, and their spending focuses on healthcare, leisure, and living expenses. Credit profiles display a long credit history and a change or transition to more conservative financial behavior. Credit scoring for retirees benefit greatly from enriched data, which provides insights into their consistent income sources and conservative spending habits.

What is AI-Based Credit Scoring and How Does it Work

AI-based credit scoring systems are changing the way banks assess the creditworthiness of customers. By applying machine learning, they analyze a vast amount of data points, far beyond what a traditional credit score would have captured. These include factors that range from spending habits to social media activity and even online behavioural patterns. This will not only enhance the accuracy of risk assessment for credit but also help financial institutions extend credit to a much larger market of customers with limited credit history.

Twisto’s approach

Twisto boosts credit scoring with its proprietary risk engine, Nikita, which uses machine learning to evaluate customer credibility based on hundreds of factors without querying traditional credit registries. After two years of development, Nikita accurately predicts customer creditworthiness using minimal input - just a name, email and other publicly available data. The system analyses online behavior, purchase history, demographic and geographic data, digital footprints, and social media profiles. This approach allows Twisto to make precise, real-time credit decisions, continually improving with each transaction.

The AI algorithms continuously learn and adapt, refining their predictive models with each new piece of data. This dynamic nature ensures that credit decisions become increasingly precise over time. Furthermore, AI-based systems can process and analyze data in real-time, supporting instant credit-scoring decisions. As we mentioned earlier, this is key for Buy Now, Pay Later (BNPL) services.

As banks increasingly turn to AI, understanding the regulatory changes and new laws becomes an important point of interest. The EU AI Act, for instance, seeks to establish a legal framework for the safe and ethical use of AI, ensuring that AI systems are transparent, non-discriminatory, and respect fundamental rights.

Learn more about the AI Act from the banking industry.

Enriched transaction data go hand in hand with AI and machine learning, creating a “whole package” for banks and their digital features. Integrating the Tapix API into your banking system is designed to be a seamless and straightforward process. The API offers comprehensive documentation and support to guide you through each step, which includes the following:

Step 1: Collect Your Data

Start by gathering payment data from all transaction sources, including card transactions, bank transfers, and open banking (PSD2) payments. Tapix handles these inputs seamlessly, ensuring comprehensive data collection.

Step 2: Call the Tapix API

Utilize the Tapix API to consolidate and enrich the raw, unstructured, and uncategorized transactional data. The API transforms this data into structured data points, sending it back to your infrastructure for further processing. One of the most interesting features is the sandbox environment, where you can thoroughly test the API with your data before implementation.

Step 3: Unlock the Potential of Enriched Transaction Data

Leverage the enriched data for analytics, user experience enhancement, sustainability initiatives, and business case development. With tools like the Tapix sandbox, you can test and optimize your data solutions effectively. Tapix offers continuous support and regular updates to keep your system up-to-date with the latest features and improvements.

Open Banking as a Lifeline to Information

Did you know? Open data usually has 2 data points, rarely more than 4. The full dataset has 9, providing three times more useful information for detecting terminals.

Apart from the enriched data itself, open banking enables banks and fintech firms to have at their disposal a broader spectrum of financial data from secure APIs. This means a more detailed analysis of a financial presence - an issue critical for a reliable measurement of creditworthiness, especially for clients without a primary account at the evaluating bank. By integrating transactional data from multiple banks, including detailed bank statements and spending patterns, open banking ensures a more accurate credit profile. This is particularly beneficial for individuals such as small business owners or gig economy workers, whose creditworthiness is currently underrepresented by traditional models.