Product insights

What Is Google Places ID and How It Improves Transaction Data

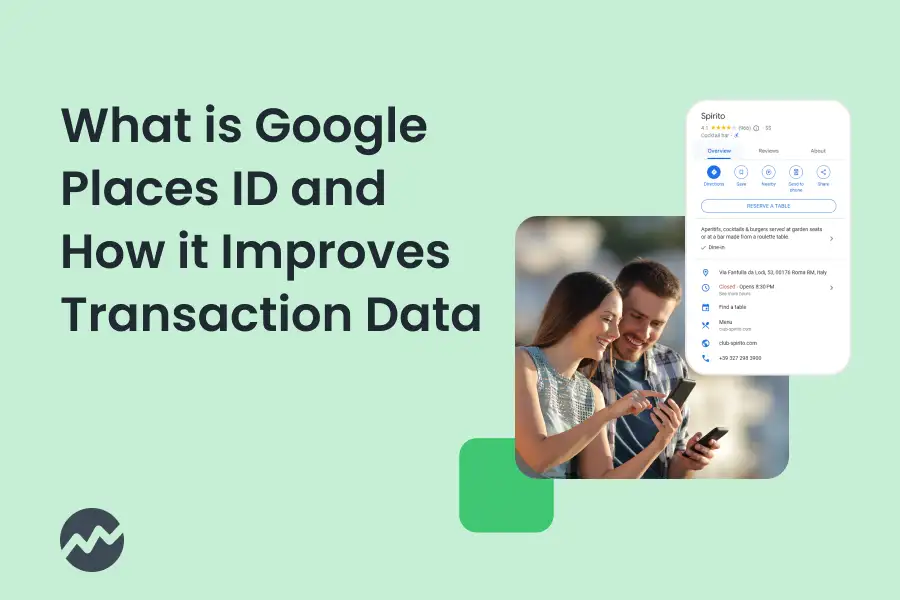

Every card payment generates a transaction record. But if you look at the raw data behind that record, you'll quickly notice a problem: the location information it contains is almost never specific enough to tell you where the customer actually was.

.webp)

Product insights

Real-Time Data Enrichment vs Batch: What Banks Need to Decide First

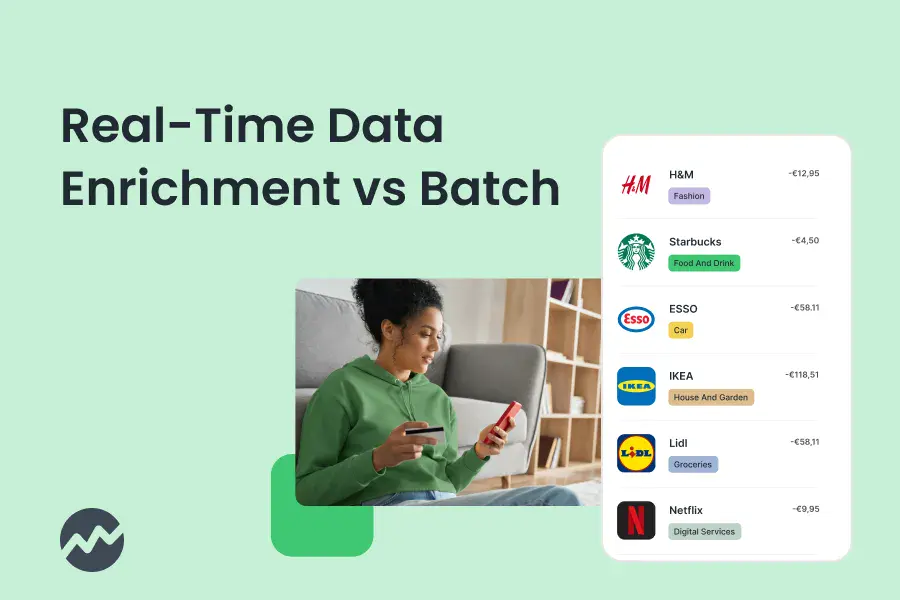

The timing of transaction enrichment determines which digital banking features a bank can realistically deliver. Getting this architectural decision right is not a backend concern - it is a product strategy decision.

Product insights

How to Choose and Integrate a Transaction Enrichment API

Most integration failures don’t happen because the API is bad. They happen because the bank treats enrichment like an additional tweak instead of a structural layer inside its transaction system. If you integrate a transaction enrichment API properly, it becomes part of your transaction infrastructure.

.webp)

Product insights

Build, Don’t Just Display: 14 Banking Solutions Influenced by Transaction Data Quality

Banks spent years treating transaction data quality as something to show. A list, a balance change, maybe a PDF statement. Now the better ones treat transaction data as something to build on: Year-in-Review recaps, subscription controls, advanced PFM, loyalty targeting, carbon footprint views. Yet the market is all over the place.

.jpg)

Product insights

How Subscription Management, Data, and Recurring Payments Drive Customer Lifetime Value

Subscription management used to be simple. You paid monthly for entertainment, maybe a gym membership, and that was the end of it. Now it’s everything. You don’t stick with a bank because the logo feels comforting or the branch is on your street. You stick because the bank becomes the default place where your financial routine works. Salary comes in. The same bills go out. The same services are renewed. After a month, your account turns into a quiet system that runs your life in the background.

Product insights

Financial Transaction Classification Categories: A Strategic Guide for Banks and Card Issuers

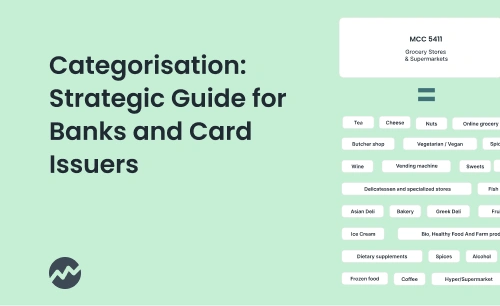

For banks, digital banks, and credit card companies, accurate transaction categorisation sits at the core of customer experience, analytics, compliance, and revenue optimisation. As consumers expect real-time insights and regulators demand clearer reporting, classification quality and proper transaction classification categories have become a competitive differentiator.

Product insights

Detection Solutions for Subscriptions: What Accurate Identification Really Requires

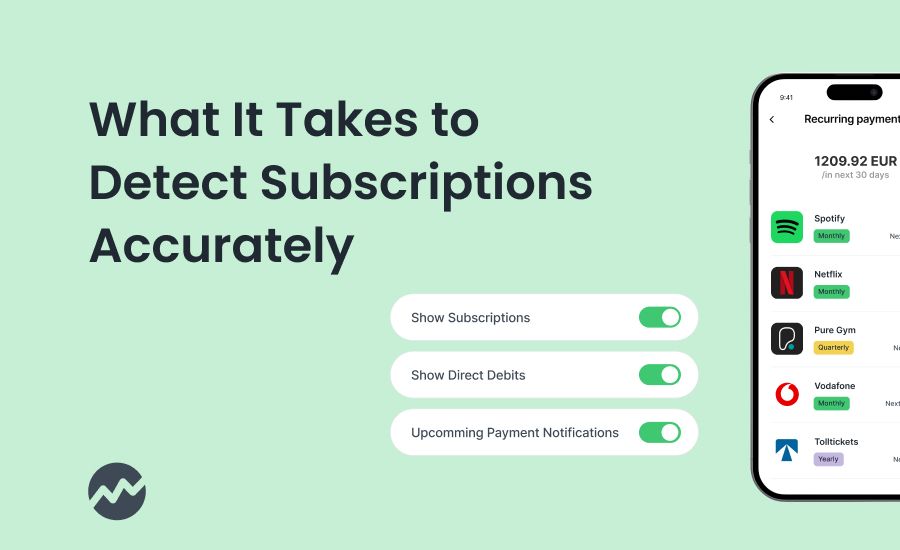

Short answer: accurate transaction data. Long answer: accurate transaction data plus the ability to treat different payment behaviours as different problems. That is the core of any true detection solution when it comes to subscriptions. Most banking apps still process transactions as one big, flat stream. But in real life, customers experience spending in three distinct ways...

Product insights

Turning Enriched Payment Information into Real Value for Banks

Enriched Payment Information works for banks and customers alike. By transforming unclear transaction codes into meaningful insights, banks earn customer trust, reduce costs, and build engagement that lasts. This technology turns a banking app into a smart financial companion that guides customers and strengthens loyalty.

Product insights

Unlocking Efficiency and Cost Savings with Payment Data Enhancement

Today, Payment Data Enhancement is integrated into almost all strategic operations. By ensuring that every transaction is accurate, complete, and intelligently validated, organisations can scale payments efficiently, reduce operational costs, and improve customer experience.

Product insights

Unique Data Points and APIs Behind Different Bank Transaction Types

Raw card data has always been half measure. You can barely read the merchant, the MCC looks “fine-ish,” and context is missing. Enrichment APIs fix that. They turn noisy payment strings into readable stories - complete with merchant identity, category, channel, location, and recurring or refund signals. The faster this happens, the better the experience for all bank transaction types. Every second of latency is a lost moment to reassure, reward, or retain a customer.

%20(1).webp)

Product insights

Improve Fraud Detection with Enriched Payment Insights

In banking, risk management is only as strong as the data it relies on. Yet most organisations still work with cryptic, incomplete, or inconsistent payment records - making fraud detection, credit scoring, and compliance unnecessarily complex. This is where payment data enhancement tools for risk management come into play.

Product insights

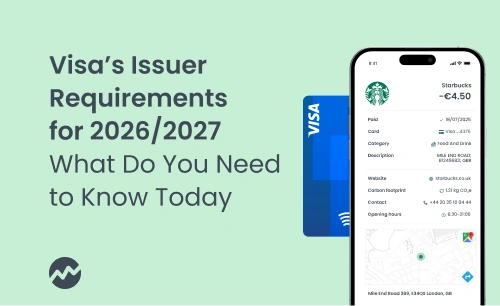

Visa Requirements to Provide Enhanced Merchant Data to Cardholders

Visa has announced a series of mandates updating how banks and fintechs manage transaction data, cardholder controls, and recurring payments. The changes follow similar regulatory steps taken by Mastercard and aim to improve transparency, consumer trust, and digital control in the European payment ecosystem.

Product insights

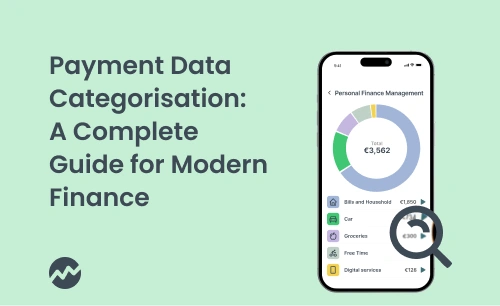

Payment Data Categorisation: A Complete Guide for Modern Finance

Every payment tells a story, but unclear codes and cryptic abbreviations often hide it. This lack of clarity leads to frustration, higher support costs, and missed opportunities. Payment data categorisation transforms messy data into structured, actionable insights, paving the way for better customer experiences and innovative financial products.

Product insights

Hyper-Personalised Banking Communication: Turning Real-Time Data into Relevant Conversations

Most people can tell when a message wasn’t meant for them. A generic “We’ve got a great offer for you” is easy to ignore. Messages that react to what a person is actually doing - this week, this morning, sometimes this minute - feel different. They feel helpful.

.png)

Product insights

How Smarter Transaction Categorisation Opens the Door to Better Banking

The way we handle financial transactions has evolved significantly. Contactless payments, mobile wallets, and digital-only banking apps have redefined what it means to manage money. Despite all the technological progress, many banks still struggle in one important area: categorising transactions effectively. This is essential for almost every digital banking service.

Product insights

Getting to Know Payment Data Enrichment in Banking: Why It’s Essential

Tracking financial flows is one of the key elements of banking, and payment data enrichment is becoming an increasingly important tool for banks to improve their services and minimise risk. In this article, we look at why it is so important in banking and how to choose a transaction data enrichment API.

Product insights

Why is Transaction Data Enrichment Important for Digital Banking?

Enhancing transaction data is essential because it helps the customers know more about their transactions through insights and additional data, which helps them make smart decisions about their financial lives and build trust with their bank, who becomes their financial partner on the life journey.

Product insights

Why Merchant Name and Logo in Digital Banking Matter More Than You Think

You’re scrolling through your bank app, trying to remember what that $33 charge was. The line says “ESO PETROL TURDA DEP”. Was that lunch? A carsharing? Did someone clone your card? You tap. You Google it. Eventually, you give up - or worse, call customer service.

Product insights

Why Hyper-Personalisation Now Defines Success in Digital Banking

Customer expectations in digital banking have evolved pretty significantly in recent years. Gone are the days when "Good morning, Alex" and a templated savings suggestion felt impressive. Today, consumers want more. They want to feel understood - not just as account holders, but as real people with complex financial habits, ambitions, and anxieties. Time for hyper-personalisation.

Product insights

Payment Data Enhancement: How to Select the Right Data Enrichment Providers for Your Business

Data is the key to understanding the customer and the long-term success of any business, so it's no wonder it's a sought-after commodity. Accurate and detailed data not only unlocks the door to further business growth, but also increases customer satisfaction.

Product insights

How to Detect Gambling Transactions in Digital Banking

It often starts small. A customer moves money into their Skrill account - nothing unusual. Just a simple transaction in the background of an otherwise quiet banking day. But hours later, that same payment is funnelled into an online casino, masked by a generic merchant category code.

Product insights

From Raw Data to Insights with Financial Data Enrichment

In today’s fintech era, it’s crucial to understand how we can use our customers’ data to make better decisions and understand their needs more deeply. But how exactly can we use this data, what types of data do we have and what can we get out of it?

.webp)

Product insights

Recurring Payments in Digital Banking: How to Go From Chaos to Clarity

The more digital we become, the more online services, subscriptions and recurring payments we need to keep track of, as they become integral part of our daily lives. From streaming platforms and cloud storages to monthly fitness memberships and car payments, these automated transactions offer convenience, but at the price. Without accurate transaction data presented in a user-friendly way, managing them becomes a financial challenge - both for consumers and banking institutions.

Product insights

How Banks Should Work with Transaction Data

For any digital banking platform to work well, transaction data needs to go beyond a simple list of payments. After all, if you can’t do the most important thing right, the rest doesn’t really make sense. Modern customers expect their financial institutions to provide clear, contextual, and visually engaging transaction details that make understanding their finances simple. Let’s explore the crucial data points and features that shape top-tier transaction details in digital banking and transform raw data into meaningful financial insights.

Product insights

The Cost of Data Inaccuracy in Digital Banking

With technology slowly progressing, data is starting to be at the heart of every transaction, decision, and strategy within banking. Whether it’s recommending financial products to users or automating decision-making processes, banks rely on data to understand their customers and provide a seamless experience. But what happens when the data is inaccurate?

Product insights

The Role of Financial Data Enrichment in PFM Tools

Personal Finance Management is designed to help consumers track their spending, set budgets, and achieve their financial goals, but in the past years, it has become much more than that. Digital banks like bunq or Tomorrow are starting to offer additional features to help customers see how their spending affects the environment around them. We are talking about checking your carbon footprint with a breakdown of spending categories, savings pockets or category restrictions for better control of your finances.

Product insights

What Makes Insightful Transaction Detail in Banking

Today, convenience and instant access to information is what makes or breaks the service. Banking has transitioned from paper statements and bank tellers to seamless digital experiences. A bank's primary touchpoint with its customers is through transaction detail – a very core of financial transparency and personal finance management. But what makes transaction details insightful and why do they matter so much?

Product insights

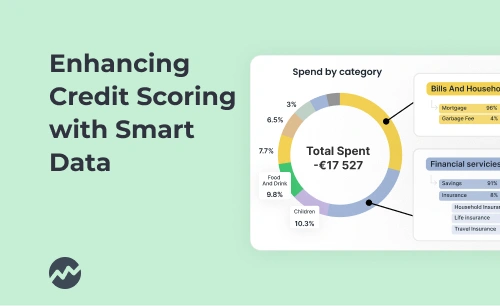

Enhancing Credit Scoring with Smart Data: The Future of Financial Risk Assessment

For many decades, credit scoring has built the foundation of financial risk assessment and provided banks and other financial institutions with a quantitative view of a borrower's creditworthiness. Traditionally, credit scores are derived from a combination of factors that include payment history, credit utilization, the length of credit history, types of credit used, and recent credit inquiries. These data points offer a very narrow window into the financial behavior of a borrower and often lead to misjudgments in lending decisions. A modern answer to this is smart data. Or, more precisely, enriched data.

Product insights

Tackling Chargebacks in Digital Banking with a Clear Payment History

Chargebacks are an important tool providing clients with the ability to dispute transactions and reclaim funds. These happen when a client contacts their bank to reverse a transaction, often because they believe the transaction was unauthorized, fraudulent, or incorrect. Chargebacks themselves also present significant challenges for merchants, banks, and fintech companies, often resulting in substantial financial losses. And the rise of digital banking has only magnified the importance of efficient chargeback management. With many automation tools available, banks need to understand that prevention is often the cheapest and smartest option available, making clear payment history more important than ever.

Product insights

Why Developer Experience Matters in Transaction Data Enrichment

Developer experience (DX) is all about making tools and services easy to use, well-documented, and supportive of developers' needs. A positive developer experience leads to: - Faster Integration: Easy-to-use portals and clear documentation reduce the time required to integrate new services.- Fewer Errors: Detailed guides and examples help prevent common mistakes.

Product insights

Cash or card? Tapix launches ATM Nearby™ to help with cash withdrawals while traveling

Learn how Tapix's new ATM Nearby ™ solution can help you improve the user experience and overall client satisfaction with your application. The world might be becoming more digital by the day, yet in many countries across the globe, there are still around 3.5 million ATMs in operation.

Product insights

Why AI chatbots depend on high quality data: Garbage in, garbage out explained

Chatbots and digital assistants are one of the emerging trends in the digital banking industry. According to Juniper research, over 80% of banks are now using some form of chatbot in customer service. Lately, more and more banks are also starting to shift to more analytical usage, such as personal assistant, which reshapes the user experience, offering personalized financial advice and assistance at the touch of a button. But every good analysis needs a well structured and organised data first.

Product insights

Business Banking (SME) Features to Build on Payment Data

Discover how Tapix revolutionizes SME banking with innovative features like GPS transaction limits, EcoTrack for environmental responsibility, or automated approvals. In the world of small and medium-sized enterprises (SMEs), there is an increasing emphasis on efficiency and innovation in financial processes.

Product insights

What is vital for a perfect PoC and how to set the right expectations

Every project in the digital banking market begins with a solution capability check. A concept that helps financial companies find the best solution for a specific use case while cooperating with the data enrichment provider that is most suitable for their needs.

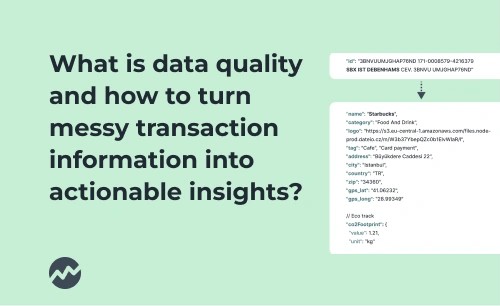

Product insights

What is data quality and how to turn messy transaction information into actionable insights?

Every transaction, every single tap with a credit card creates a stream of 0 and 1, and the ability to extract meaningful insights from that data is a key differentiator for banks and fintech companies.

Product insights

Why Allocating a Budget for Mastercard AN 4569 Compliance Is Crucial in 2024

Discover the strategic importance of allocating a budget for Mastercard AN 4569 compliance. Enhance user trust, mitigate risks, and gain a competitive edge in digital finance.

Product insights

In-house vs. Third-party Solutions for Mastercard AN4569 Compliance: Making the right choice

Explore the pros and cons of in-house development vs. third-party solutions for Mastercard AN4569 compliance. Make the right choice for your business's payment data enrichment journey.

Product insights

Mastercard AN4569 Best Practice: Elevating User Experience with Visual Data Showcase

Enhance your user experience by meeting Mastercard AN4569 requirements. Elevate UI design, showcase visual data, and meet revised standards for enriched payment data

Product insights

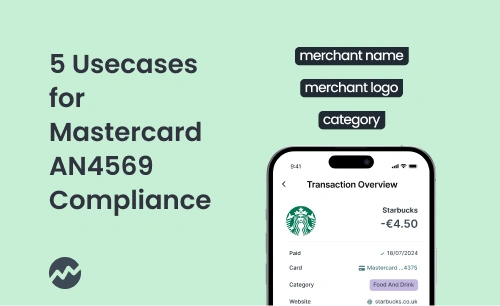

5 Usecases for Mastercard AN4569 Compliance Beyond Minimum Requirements

Explore 5 use cases for Mastercard AN4569 compliance that go beyond minimum requirements. Unlock key insights for enhanced analytics, and customer-centric financial services.

Product insights

Mastercard AN4569 Compliance Guide for Banks

Discover essential strategies for banks to meet Mastercard mandate AN4569. Optimize compliance and get the most out of this requirement.

Product insights

Why Payment Data is the Key to Unlocking the New Value for Customers

In today's digital age, data is more than just information. It is a strategic asset that can unlock the immense value behind it. The aphorism that data is the gold of the 21st century applies here. One area where this trend is particularly evident is the world of payment data.

Product insights

Enhanced payment data with new Mastercard rules: nice-to-have? A must-have from October 2023!

Data is the most valuable commodity of the 21st century, and its importance is growing daily across industries. Finance and payments are good examples of this. Find out what the new Mastercard Mandate means for banks and fintechs.

Product insights

Data Enrichment & Analytics from Payment Data: The Key to Optimal Banking App Functionality

How do you improve your digital banking app? Data is a key resource in this regard. Through data enrichment and subsequent analytics, banks can gain a deeper understanding of their customers, optimize their operations and come up with new opportunities for their customers. In this article, we will focus on leveraging the underlying data from MCC codes and enriching it. This knowledge is one of the pillars of the success of neobanks like bunq or Revolut, so don’t be left behind.

Product insights

How to Cross-sell through enhanced card payment data

Have you ever hesitated to go into a car dealership for fear of being mobbed by hungry salesmen? Bank account holders feel the same way about banks that are too aggressive with cross-selling efforts. Rather than taking a scatter-shot approach that catches customers in the crossfire, banks should target those customers who might buy the product.