Don’t feel like reading? Listen to the audio version.

The more digital we become, the more online services, subscriptions and recurring payments we need to keep track of, as they become integral part of our daily lives. From streaming platforms and cloud storages to monthly fitness memberships and car payments, these automated transactions offer convenience, but at the price. Without accurate transaction data presented in a user-friendly way, managing them becomes a financial challenge - both for consumers and banking institutions.

The Rise of Subscription Economy

Subscriptions are no longer limited to entertainment services like Netflix or Spotify. Today, nearly every industry has adopted a subscription model. From grocery delivery services to professional SaaS tools, the subscription economy is booming - in 2024, the market was valued at $166.69 billion, with projections suggesting it will reach $182.94 billion in 2025, growing at a compound annual growth rate (CAGR) of 9.7%.

From a bank’s perspective, the scale is even more striking: between 15% and 50% of all card transactions processed by a typical European bank are recurring in nature. That means as many as half of all transactions a bank processes today are part of an ongoing relationship between a customer and a merchant - yet most banks have no system to recognise, track, or surface that relationship to the customer.

But as subscriptions have become more common, they have also become more difficult to track. A single household might have a dozen active subscriptions at any given time. Many forget about some, others struggle to cancel them, and some unknowingly sign up for services they never intended to keep. The rapid expansion of this payment model has made financial oversight more crucial than ever, and banks need enhanced transaction data from providers like Tapix to stay on top.

For them, failing to offer subscription management solutions means missing out on opportunities to protect payment volumes, as frustrated customers cancel their cards entirely to stop unwanted subscriptions rather than removing individual merchants. Moreover, a proper system for these payments also boosts card-on-file transactions, keeping the bank’s payment methods top of mind, strengthening customer loyalty.

Did you know?

In the UK, nearly 10 million active subscriptions are unwanted, costing consumers approximately £1.6 billion annually.

First of all, not all recurring payments are subscriptions, though they are often treated as the same. Recurring payments are any automated transactions where a customer authorises funds to be deducted on a scheduled basis - weekly, monthly, or annually. These include essential expenses such as rent and mortgage payments, utility bills, car lease or insurance premiums.

Subscriptions, on the other hand, are a subset of recurring payments that grant ongoing access to a product or service. Streaming services, fitness memberships, digital content platforms, and cloud storage solutions all fall under this category. While subscriptions represent a rapidly growing part of recurring payments and a simple tag in banking app is sufficient, banks must recognise that enriched transaction data applies beyond just subscriptions - it enhances clarity for all types of recurring charges.

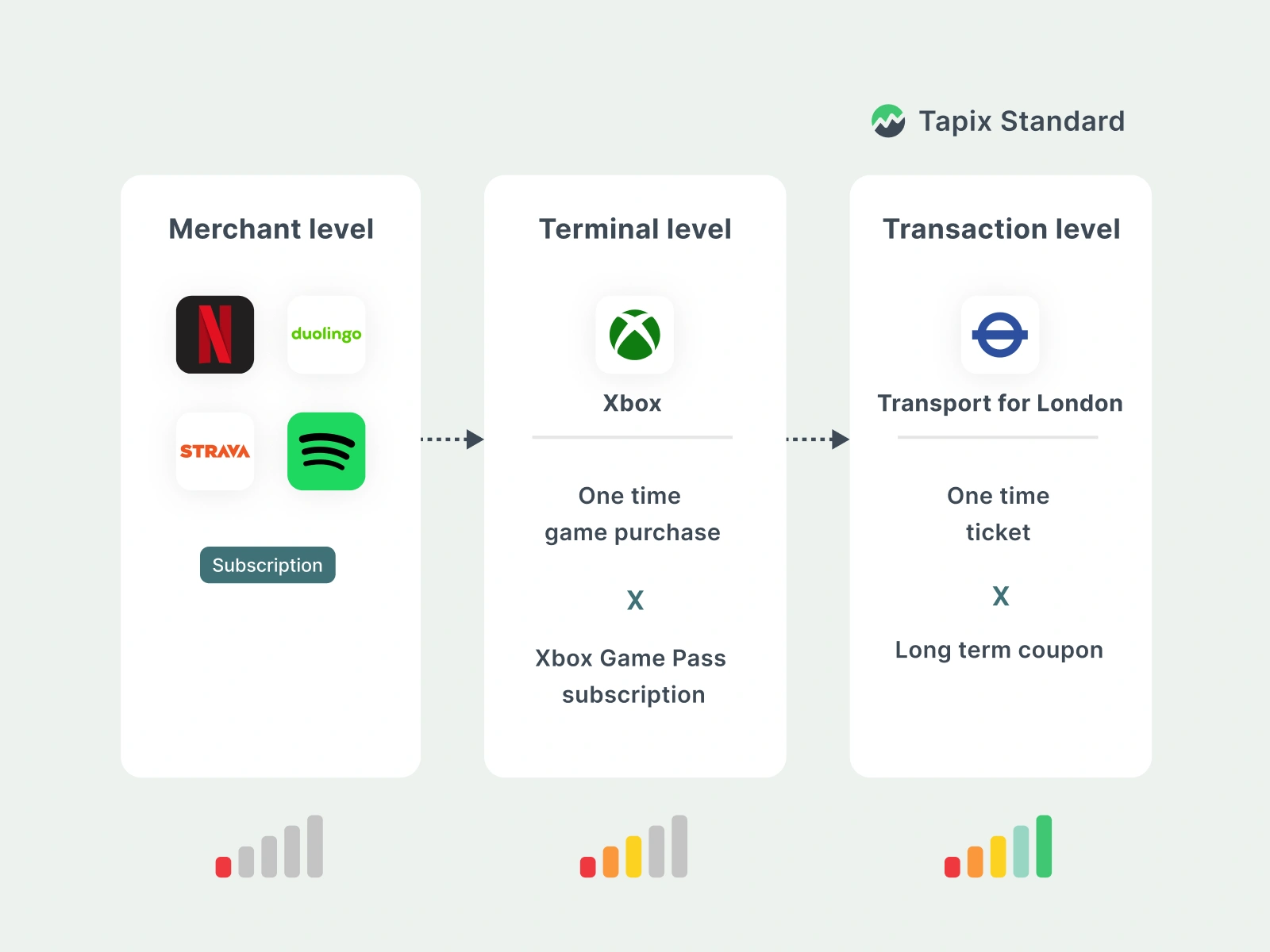

For that, you need recognition on a transaction level, not just merchant level, as shown in the infographic above. Since many one-time payments are hidden within actual subscription-based services, a bank needs to know when a user has made a one-time payment (YouTube channel support) and when it’s an actual recurring payment (a YouTube monthly subscription).

Take control of recurring payments with Tapix's Recurring Payment Intelligence. Learn more today!

How Banks Can Identify and Manage Subscriptions

Subscription management starts with identification. Before a bank can help customers track their subscriptions, it must first recognise them as such. This requires proper categorisation and merchant recognition. To streamline subscription tracking, banks need to integrate enhanced transaction data that includes. Key indicators that a transaction is a subscription include:

- Merchant type: Streaming services, SaaS providers, and membership platforms.

- Payment frequency: Recurring patterns (monthly, quarterly, annual billing cycles).

- Billing descriptors: Many transactions lack clear labels, requiring data enrichment to clarify merchant information.

There is an important point here: labelling at the merchant level is not sufficient. A merchant like Apple processes both one-time app purchases and recurring iCloud subscriptions. The London Underground handles both single-journey tickets and monthly travelcards. Without transaction-level recognition, a bank either labels all of a merchant’s transactions as subscriptions (creating false positives) or none of them (missing real subscriptions entirely). Only transaction-level analysis can separate the two accurately.

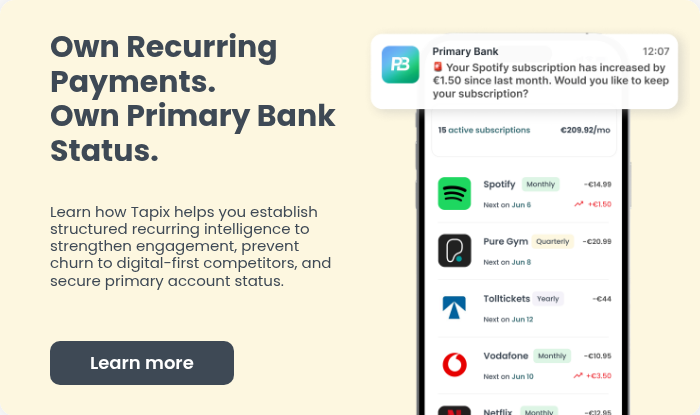

Without enriched transaction data, users see cryptic entries on their bank statements - descriptions like *"Spotify P348676F6A" or "Microsoft36" - leaving them unsure about the charge. With proper enrichment, these transactions become clear: "Spotify Premium - Monthly Subscription" or "Microsoft Office 365 - Annual Payment". This small shift dramatically improves user experience and financial awareness

The Role of Enriched Data in Recurring Payments

To start moving in the right direction, financial institutions need to understand how important accurate enhanced transaction data is to this entire process. This involves augmenting basic transaction details with additional information, providing a comprehensive view of each payment.

To streamline subscription tracking, banks need to integrate enhanced transaction data that includes:

- Merchant Name & Category – Clearly identifying service providers.

- Payment Frequency – Whether it's billed monthly, quarterly, or annually.

- Next Billing Date & Amount – Helping users anticipate and budget for upcoming charges.

- Automatic Charging Indicator – Showing whether a payment will renew automatically.

- Constant Amount Detection – Identifying price hikes or unexpected fees.

Tapix delivers this enrichment layer at scale - over 2 billion transactions enriched per month, across 96+ active markets, with 99.99% data accuracy. That coverage matters because recurring payments are fragmented across thousands of merchants, many of which are not flagged as subscription providers by scheme data. Identifying them requires a model trained on real behavioural patterns at this volume.

With Recurring Payments Intelligence, banks can provide a clear and structured overview of a customer’s recurring financial commitments, reducing disputes and improving trust in digital banking services.

Why this matters?

Consumers often sign up for free trials but forget to cancel them before being charged. According to a 2024 survey, 42% of consumers admitted to paying for a subscription they no longer use simply because they lost track of it.

Banking apps that utilise enriched transaction data can automatically categorise transactions as:

- Recurring Payments (e.g., Netflix, Amazon Prime, Microsoft Office 365, gym memberships).

- Fixed Bill Payments (e.g., mortgage, rent, utility bills).

- One-Time Transactions (e.g., online purchases, restaurant bills).

By providing a clear view of recurring payments, subscriptions, or direct debits, banks can predict future spending and assess customers' ability to meet financial obligations. This proactive management is crucial, as Forrester estimates that subscription-related disputes alone cost banks $136 million annually.

Banking Innovations in Subscription Management

Recognising the complexities consumers face with recurring payments, banks and fintech companies have introduced innovative solutions. Here's an in-depth look at how Revolut and bunq addresses subscriptions:

Subscription Overview: Revolut's 'Subscriptions' feature provides users with a centralised view of all their recurring payments, including subscriptions, direct debits, and scheduled payments. This unified dashboard enables customers to monitor how much they are spending on each service and with each merchant, promoting better financial awareness.

- bunq provides a feature that allows users to view and manage their subscriptions directly within the app. This functionality offers insights into recurring expenses, enabling users to monitor and control their financial commitments effectively.

Real-Time Notifications: To ensure users maintain control over their finances, Revolut sends notifications before scheduled payments are due. These alerts inform customers about upcoming charges, allowing them to manage their account balances proactively. Additionally, if there are insufficient funds to cover a payment, Revolut notifies users in advance, providing time to top up their accounts or decide on alternative actions.

- To help users stay informed about their financial activities, bunq sends real-time notifications for upcoming payments and renewals. This proactive approach ensures that customers are aware of their obligations and can manage their accounts accordingly.

Merchant Blocking: Revolut users can manage their subscriptions directly through the app by having the ability to block or unblock payments to specific merchants. If a customer identifies an outdated or unwanted subscription, they can swiftly block future payments without the need to contact the merchant or navigate complex cancellation processes. This feature simplifies subscription management and helps prevent unnecessary expenses.

Enhanced Detection Mechanisms: Utilising crowdsourcing, Revolut's detection system allows users to flag recurring payments that may not have been automatically identified by the app. This collaborative approach ensures that the subscription management feature remains accurate and up-to-date.

Beyond Subscriptions with Enriched Data

While subscription tracking is a new major trend banks need to adopt, the potential of enriched transaction data extends far beyond digital services and entertainment. Banks can use these insights to improve financial transparency across various types of recurring payments:

- Rent & Mortgage Payments – By tracking patterns in housing payments, banks can offer timely reminders, detect missed payments, and provide better budgeting tools.

- Toll Tag & Transportation Payments – Many consumers rely on auto-replenishment for highway tolls or metro passes. Enriched data can help track these expenses, avoiding overdrafts or unexpected charges.

- Business Banking Subscriptions – Companies often struggle to manage recurring vendor payments. A robust tracking system can categorize expenses, flag duplicate services, and streamline accounting.

Another growing trend is the use of virtual cards for subscription management. Some digital banks, including Partners Banka, have introduced features that allow users to track where their virtual card details are stored online. This is a game-changer for managing online payments.

Real deployments confirm the gap that enrichment closes. In the Czech market, Tapix’s pattern-based detection identified 200 additional subscription merchants on top of 400 already known through traditional classification. These included Prague public transport, Wolt, Foodora, and Rohlik.cz - none of which would have been captured by a standard merchant-category approach. Notably, while yearly subscriptions represented only 2% of transaction count, they accounted for 31% of total subscription spend - demonstrating that low-frequency, high-value recurring payments are disproportionately important to surface.

By integrating Tapix’s Recurring Payments Intelligence, financial institutions can turn confusion into clarity - helping customers take back control of their financial commitments while strengthening their position as primary banking providers.