Today, convenience and instant access to information is what makes or breaks the service. Banking has transitioned from paper statements and bank tellers to seamless digital experiences. A bank's primary touchpoint with its customers is through transaction detail – a very core of financial transparency and personal finance management. But what makes transaction details insightful and why do they matter so much?

Transaction details are the backbone of personal finance. They tell the story of where your money goes, what you prioritize, and how you manage your finances. With the rise of digital banking, people have become more engaged with their financial data. It’s not just about balance, but also understanding spending habits, tracking budgets, and ensuring financial health.

Did you know? According to Accenture research, 46% of consumers aged 18-24 often lose track of their financial products and services, compared with 18% of those aged over 65.

But this only works when the transaction details provided are clear, accurate, and informative. And this is where it gets interesting.

The Problem with Raw Transaction Data

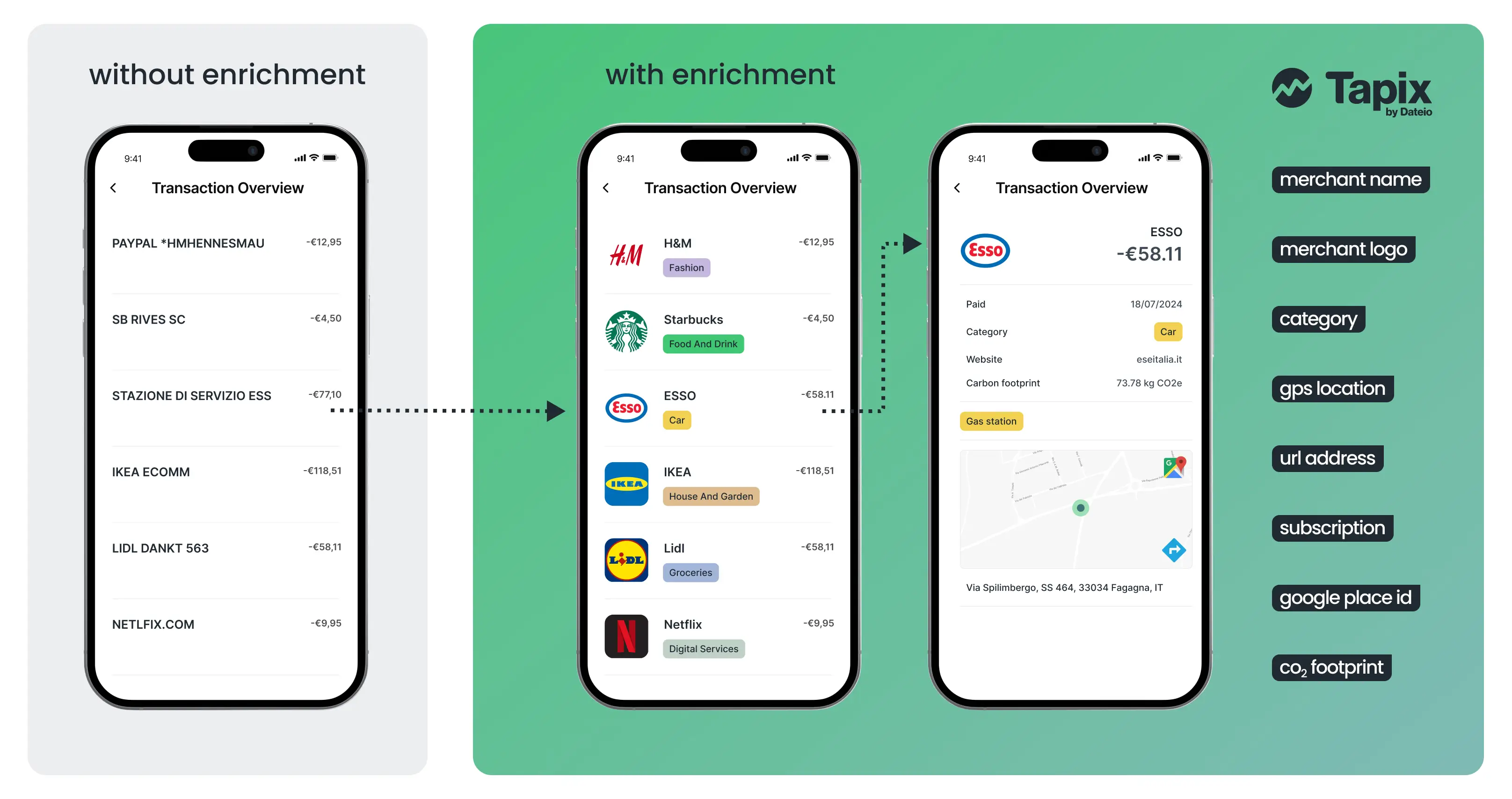

Imagine you’re scrolling through your bank statement and see a charge from “SB RIVES SC”. You vaguely remember making a purchase, but the description is so unclear that you’re left unsure. What was this payment for? Was it a necessity or an impulse buy? Was it even authorized? The ambiguity of non-enriched transaction details leaves much to be desired, and many banks still use this structure for their financial ecosystems. In its raw form, banks usually get very basic information like terminal and merchant ID, a simple description, the city where the payment occurred and a basic Merchant Category Code. With only 63% of MCC data being correctly categorised, it is barely usable and not very informative. Luckily, there is a way to level up those data.

Contrast this with the enriched transaction details that providers like Tapix can add to those raw data. The entry might read: “Starbucks - Food and Drink”. Suddenly, the charge is not only recognizable but also categorised, allowing you to understand your spending at a glance. Enriched transaction data offers context by providing accurate merchant names, logos, locations, labelling, Google Places ID and even categorising expenses automatically. This clarity is essential for budgeting, tracking subscriptions, or identifying fraudulent activity. It serves as a foundation everything else can firmly stand on.

Many banks and fintechs utilize in-house teams to handle transaction data, which drains financial resources and time. Much more suitable option is to simply integrate an external provider´s API. The latter option saves time and ensures the highest possible data quality thanks to the provider´s expertise. A good example of such transition is Dutch fintech bunq, which first handled merchant logo database and basic categorisation in-house. Later, bunq implemented Tapix´s data enrichment solution with clear transaction detail overview, high-quality logos, and accurate categorisation labelling for recurring payments, bringing real-time financial insights to all app users.

Learn more about this transition through the success story of Dutch fintech bunq

Enriched Transaction Details

To understand the value of enriched transaction details, let’s investigate what makes up a payment. Every time you swipe your card or click “buy,” a wealth of data is generated. This includes not just the amount and merchant name but also details like terminal and merchant ID, simple merchant description, city or country where the payment took place and a basic MCC code. With raw data processed in-house, banks can mostly get a correct logo and merchant name out of it, which is not very usable in the wider financial context. Enriched transaction data go beyond those basic Merchant Category Codes.

Using the external enrichment API from providers like Tapix turns simple, often cryptic information into a valuable piece of data. Going to a shop level, banks get not only accurate logo and merchant name but also correct category, store type, tags, address with Google Place ID or website URL. Such accuracy reduces confusion and creates accurate data that can be used in a variety of ways, from detailed transaction overviews to other solutions, like hyper-personalisation, credit scoring or PFM 2.0 tools. According to a report by McKinsey, 56% of consumers expect their bank to offer tools that help them manage their money more effectively, and enriched transaction data is a critical part of this too.

Let’s break down how each data point can be enriched to add maximum value.

Merchant Name

When you see a transaction on your statement, the merchant name is often the first point of reference. However, non-enriched transaction data can present merchant names in a confusing or incomplete format. For example, “AMZ*12345” might appear instead of “Amazon Marketplace”, “Amazon” might actually be “Amazon Prime” while “PayPal” in the context of payment gate can be “eBay” altogether. Enriching the merchant name ensures that customers see a clear and recognisable name. If a merchant is not categorised correctly, it can lead to inaccurate data all along the line.

Merchant Logo

A merchant logo is an important visual cue that helps users quickly identify where they’ve made a purchase. However, simply adding a logo isn't enough - accuracy and consistency are key. An enriched data point will provide a high-resolution logo, typically optimized at 512x512 pixels, perfectly formatted for circular displays, which are standard in most banking apps today.

Transaction Categorisation

Automated systems often miscategorize transactions, leading to inaccurate budget analyses. Enriching transaction categorisation goes far beyond regular MCC codes and allows users to see their spending broken down into accurate, well-defined categories, such as “Groceries” or “Utilities”. With Tapix, categorisation gets 25 categories, 500+ unique tags and 99.99% data accuracy.

GPS Location

GPS location data adds a geographical context to transactions, allowing users to see exactly where a purchase was made. This feature is particularly valuable in combating fraud, as it allows users to quickly identify transactions that occur in unexpected locations. Tapix offers 1.5 million unique locations and 454k+ recognised merchants.

URL Address

Including the merchant’s URL address in a transaction record offers users an easy way to revisit the merchant’s site, especially useful for online purchases. This enrichment not only adds convenience with language-localized specifics but also enhances security, as customers can verify the legitimacy of the merchant.

Subscription Labeling

Enriching transaction data with subscription labels allows customers to see which transactions are tied to ongoing services, helping them manage and, if necessary, cancel subscriptions with ease. This feature also helps users to track how much they are spending on subscriptions over time, contributing to better financial management.

Did you know? A survey conducted by Accenture found that over 47% of customers said they would consider switching banks if another provider offered better digital tools and services.

Who Does It Right?

Several banks and fintech companies are setting a new standard when it comes to transaction data and their use. Take Monzo, a UK-based digital bank, for example. Monzo’s mobile app doesn’t just list transactions; it breaks them down with merchant logos, categories, and even allows users to add notes or attach receipts to each transaction. This level of detail provides users with a comprehensive view of their spending. With features like changing transaction categories, users can reclassify their spending, ensuring their budgets reflect their personal priorities. This not only enhances the accuracy of financial reports but also empowers customers to take control of their finances.

Similarly, Revolut goes a step further by offering real-time notifications that include enriched transaction details as soon as a purchase is made. These notifications are not just about listing the amount spent; they incorporate enriched data like merchant details, location, and even currency conversion if applicable. This immediate feedback loop keeps users engaged and informed, reducing the anxiety of waiting for transactions to post. Revolut also allows users to adjust transaction amounts for analysis, since not all transactions are straightforward. For instance, a payment might include a one-time discount or a portion that’s reimbursed later. Letting users adjust the amount used in budget calculations or spending analysis ensures that their financial reports are accurate and personalised.

Did you know? According to a study by Forrester, customers who use banks with advanced digital features are 31 % more likely to recommend their bank to others.

Incorporating live feedback mechanisms enables users to instantly flag suspicious activity or errors. This feature enhances security and builds customer trust, as banks can swiftly respond to potential issues. Moreover, both Monzo and Revolut are constantly adding new features connected to additional data points such as recurring payments, loyalty rewards, and environmental impact scores. For instance, users might see not just the cost of their coffee but also how many loyalty points they earned.

By building a foundation of enriched transaction data, banks can unlock a host of features that not only improve customer satisfaction but also drive loyalty and engagement. Accurate transactions affect many layers of mobile banking and the entire ecosystem.